Case Summary: Foss v. Harbottle 1843

In short

Court of Chancery (Wigram VC, 1843): two principles — (1) the company is the proper plaintiff for wrongs done to it; (2) if a majority can ratify the act complained of, the court will not interfere at the suit of a minority. Four exceptions: fraud on minority (wrongdoers in control), ultra vires acts, special majority required, personal rights of shareholders infringed. Indian equivalent: §241 Companies Act 2013 (oppression/mismanagement) and §245 (class action).

In this brief

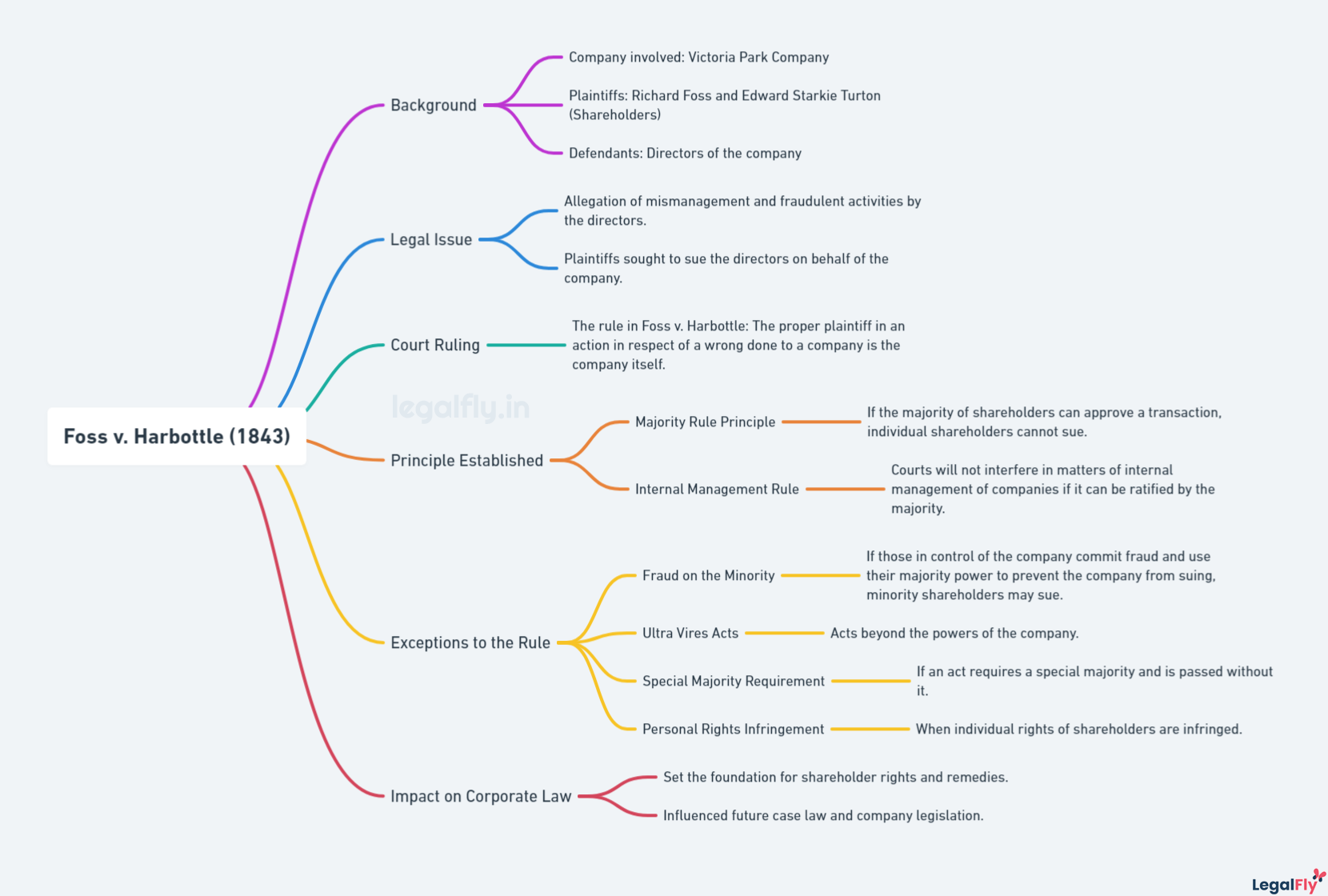

Background and Facts

The Victoria Park Company was incorporated in 1837 to develop a public park on the outskirts of Manchester. Richard Foss and Edward Turton, two minority shareholders, brought an action in the Court of Chancery against the company's promoters and directors — Thomas Harbottle and others — alleging mismanagement and fraud.

The allegations included: the directors had improperly mortgaged company land and applied company property to improper purposes; company documents bore forged seals; and land had been sold at undervalued prices to discharge the improper mortgages. The defendants argued that the majority shareholders had ratified (or could ratify) the transactions, and that in any event the individual shareholders had no standing to sue for wrongs done to the company.

Holding

Sir James Wigram V-C dismissed the action. He articulated two principles that together form the rule in Foss v Harbottle:

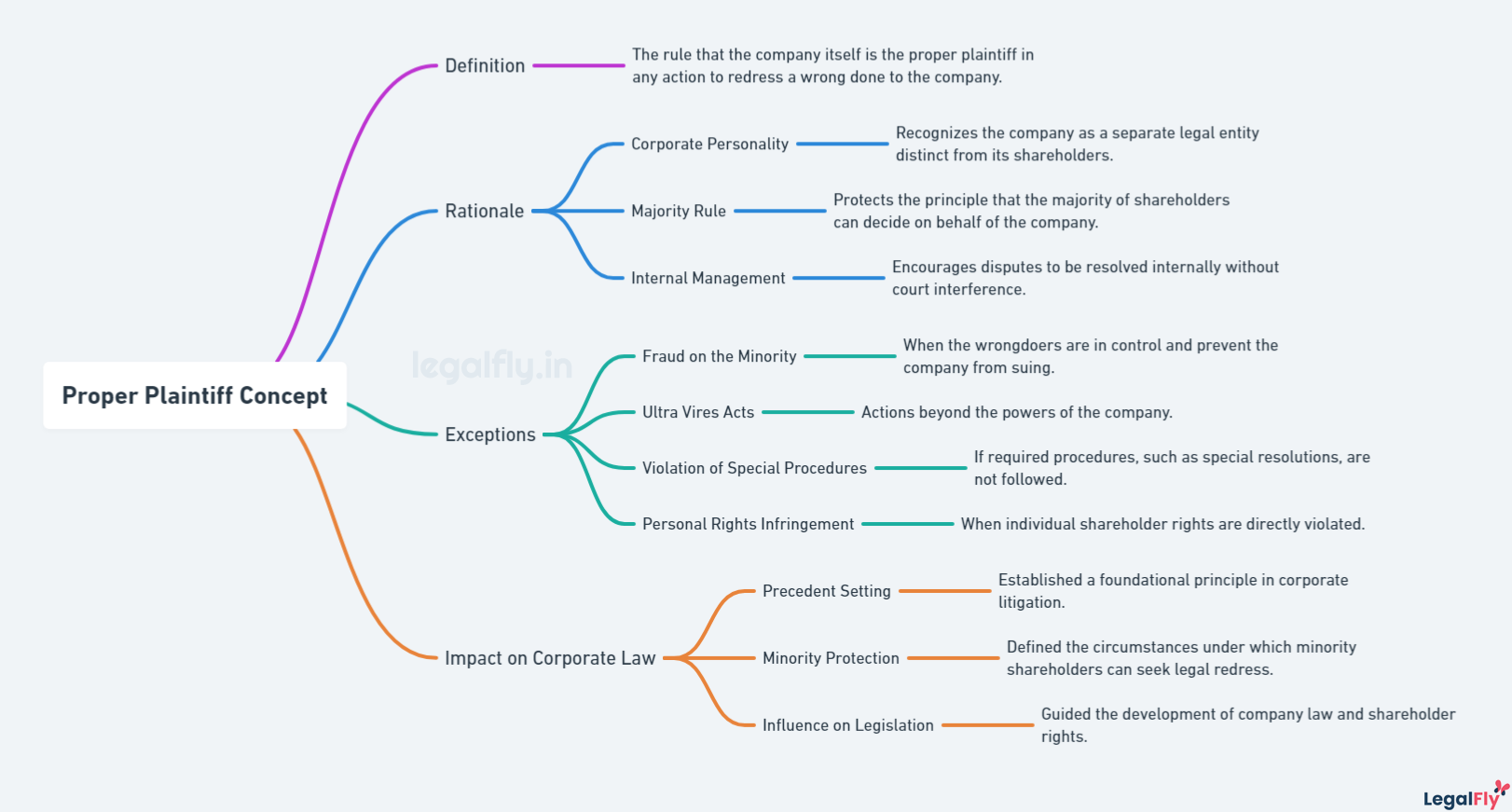

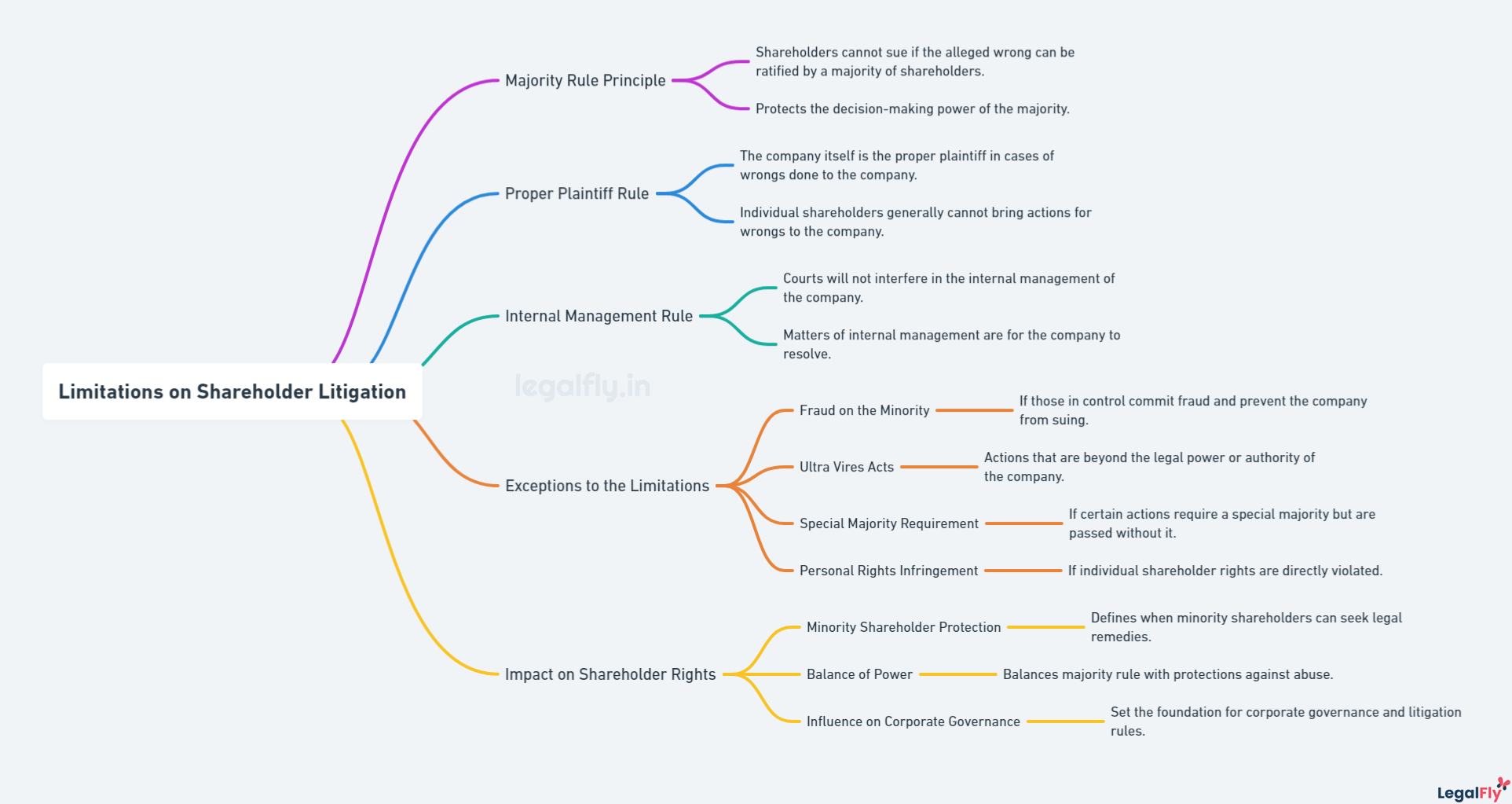

Principle 1 — The Proper Plaintiff Rule

The company itself is the proper plaintiff in an action for a wrong alleged to have been done to it. Individual shareholders have no standing to sue on the company's behalf unless specific exceptions apply. A company is a legal entity distinct from its members; harm to the company is to be redressed by the company, acting through its organs.

Principle 2 — The Internal Management / Majority Rule

Where the alleged wrong is one that the majority of shareholders can lawfully ratify, the court will not interfere at the suit of a minority. A court of equity does not allow a suit to be maintained on behalf of the company if the act can be confirmed by a simple majority vote — the minority must yield to the majority's commercial judgement.

The Four Exceptions

Later cases developed four recognised exceptions where a minority shareholder may sue notwithstanding the Foss v Harbottle rule:

| Exception | When it applies | Example |

|---|---|---|

| 1. Fraud on the minority | Wrongdoers are themselves in control of the company and will prevent it from suing | Directors divert company assets to themselves and hold a controlling majority |

| 2. Ultra vires or illegal acts | The act is beyond the company's legal capacity or is illegal; majority cannot ratify | Company acts outside its objects clause |

| 3. Special majority required | The act requires a special or extraordinary resolution but was passed by a bare majority only | Alteration of articles requiring 75% vote passed by 51% |

| 4. Personal rights of shareholders | The wrong is directly to the shareholders' own rights, not merely to the company's | Wrongful refusal to register a share transfer; deprivation of voting rights |

Derivative Actions

The modern derivative action codifies the "fraud on the minority" exception: a minority shareholder sues in the company's name (deriving their right from the company) when wrongdoers are in control. In England, derivative claims are now governed by the Companies Act 2006 (§§260–264), replacing the old common-law exception with a statutory permission stage.

Indian Law

The rule in Foss v Harbottle is recognised by Indian courts and has been considered in several High Court judgments. The Companies Act, 2013 now provides statutory remedies that parallel the exceptions:

- §241 — Oppression and mismanagement: any member may apply to the National Company Law Tribunal (NCLT) if the company's affairs are being conducted in a manner prejudicial to the members or public interest.

- §245 — Class action suits: 100 members (or 5% of total members, whichever is less) may file a class action for fraud, mismanagement, or breach of duty. India's first statutory derivative/class action provision.

- §34 / §36 — Fraudulent misrepresentation in prospectuses; suitable for wrongs to new shareholders.

Significance

- Corporate personality: Foss v Harbottle reinforces Salomon's principle that a company is a separate legal person. Claims for corporate wrongs belong to the company, not its members.

- Majority rule: The case underpins democratic governance in companies — disputes are resolved by shareholder votes, not litigation by individual members.

- Tension with minority protection: The rule's strictness gave rise to elaborate exceptions and, ultimately, statutory reform; it frames the perennial debate between majority efficiency and minority accountability.