Section 138 of the Negotiable Instruments Act: Cheque Bounce Law

In this article

- Overview of Section 138

- Legal Framework of Section 138

- Provisions Under Section 138

- Criteria for a Cheque Bounce Under Section 138

- Penalties and Legal Repercussions

- Legal Procedures and Requirements

- Notice Requirement for Dishonoured Cheques

- Legal Process for Recovery and Penalties

- How to legally respond to a cheque bounce incident under Section 138?

- Impact and Importance of Section 138

- Protecting Creditor's Rights

- Deterring Financial Misconduct

- Critical Analysis and Case Studies

- Recent Amendments and Legal Debates

- Conclusion

Overview of Section 138

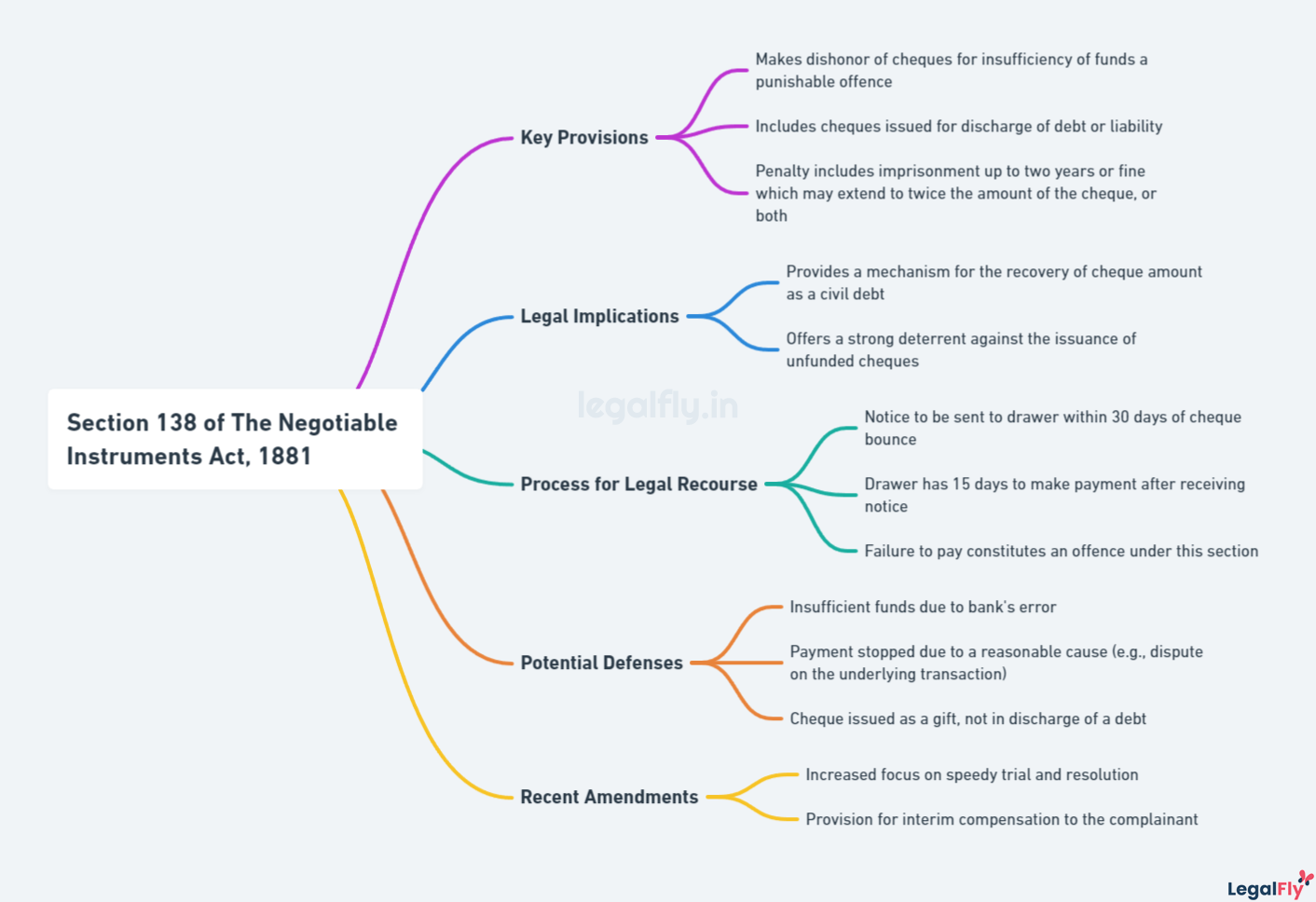

Section 138 of the Negotiable Instruments Act, 1881 makes it a criminal offence to issue a cheque that is later dishonoured for insufficiency of funds (or because it exceeds the arrangement made with the bank), where the cheque was given to discharge a legally enforceable debt or liability. It was inserted by the Banking, Public Financial Institutions and Negotiable Instruments Laws (Amendment) Act, 1988 and came into force on 1 April 1989, with the aim of restoring faith in the cheque as a mode of payment.

Although a cheque-bounce case is filed and tried as a criminal matter, it is essentially quasi-civil in nature: the dominant object is to compensate the payee and recover the cheque amount rather than simply to punish the drawer. The provision applies to cheque transactions across India and gives the payee a clear, time-bound route to hold a defaulting drawer accountable.

Section 138 works alongside a cluster of supporting provisions: Section 139 (presumption that the cheque was issued for a debt or liability), Section 141 (offences by companies), Section 142 (who may complain and the time limit), Section 143 (summary trial), and Sections 143A and 148 (interim compensation and appellate deposits, added in 2018). Together they form India's cheque-bounce framework.

Legal Framework of Section 138

Section 138 applies only when a cheque is returned unpaid because the funds in the drawer's account are insufficient, or because the amount exceeds the arrangement (such as an overdraft limit) agreed with the bank. Dishonour for unrelated reasons — for example, a genuine signature mismatch on a cheque not issued for a debt — may not attract the section.

- It covers cheques only, not other negotiable instruments such as bills of exchange or promissory notes.

- The cheque must have been issued for the discharge of a legally enforceable debt or other liability, in whole or in part. A cheque given as a gift or for an unenforceable claim is outside Section 138.

- The cheque must be presented to the bank within its validity period — currently three months from the date it bears (cheques are valid for three months under RBI directions).

- The offence is non-cognizable, bailable and compoundable. The police cannot register an FIR or arrest the drawer; the case proceeds as a private complaint before a Magistrate, and the parties may settle (compound) it at any stage under Section 147.

Since the Negotiable Instruments (Amendment) Act, 2015, territorial jurisdiction is fixed by Section 142(2): the complaint is tried by the court where the branch of the bank in which the payee maintains the account (the collecting bank) is situated. This legislatively reversed the earlier position in Dashrath Rupsingh Rathod v. State of Maharashtra (2014), which had tied jurisdiction to the drawer's bank.

Provisions Under Section 138

Section 138, read with Sections 142 to 148, lays down the ingredients of the offence, the mandatory timeline, and the penalties for a dishonoured cheque.

Criteria for a Cheque Bounce Under Section 138

For the offence to be made out, every one of the following ingredients must be satisfied:

- A cheque was drawn by the drawer on his own bank account for payment of money to the payee.

- The cheque was issued to discharge a legally enforceable debt or liability, in whole or in part.

- The cheque was presented to the bank within three months (its validity period).

- The bank returned the cheque unpaid for insufficiency of funds or because the amount exceeded the arrangement.

- The payee issued a written demand notice within 30 days of receiving the bank's cheque-return memo.

- The drawer failed to pay within 15 days of receiving that notice.

The cause of action arises only when the drawer fails to pay within the 15-day window. The complaint must then be filed within one month of that date under Section 142, though the court may condone a delay for sufficient cause.

The table below sets out the statutory clock that a payee must follow.

| Stage | Event | Time limit |

|---|---|---|

| Presentation | Deposit the cheque with the bank | Within 3 months of the cheque date (validity period) |

| Demand notice | Payee sends written demand after the cheque-return memo | Within 30 days of receiving the dishonour intimation |

| Payment window | Drawer's chance to pay the cheque amount | 15 days from receipt of the notice |

| Cause of action | Arises if the drawer does not pay in 15 days | On expiry of the 15-day window |

| Filing the complaint | Payee files a complaint before the Magistrate | Within 1 month of the cause of action (Section 142) |

Penalties and Legal Repercussions

On conviction under Section 138, the court may impose:

- Imprisonment for a term which may extend to two years; or

- A fine which may extend to twice the amount of the cheque; or

- Both imprisonment and fine.

In practice, courts often direct the drawer to compensate the payee — frequently the cheque amount plus interest and costs — rather than imposing a jail term, reflecting the compensatory purpose of the provision. Under Section 143A, the Magistrate may also order the drawer to pay interim compensation of up to 20% of the cheque amount even before conviction, and under Section 148 an appellate court may require an appellant convicted under Section 138 to deposit a further 20% of the compensation before the appeal is heard. Both provisions were introduced by the 2018 Amendment to curb delay.

Legal Procedures and Requirements

When a cheque bounces for insufficient funds, the payee or holder in due course may prosecute the drawer under Section 138. The section and Section 142 set out the steps that must be completed for a valid case.

Notice Requirement for Dishonoured Cheques

The payee must send a written demand notice to the drawer within 30 days of receiving the bank's intimation that the cheque has been returned unpaid. The notice must clearly demand payment of the cheque amount. The drawer then has 15 days from receiving the notice to pay. Only if the drawer fails to pay within those 15 days does a cause of action arise, allowing the payee to file a complaint. A defective or premature notice can defeat the complaint, so its contents and timing matter.

Legal Process for Recovery and Penalties

If the drawer does not pay within 15 days of the notice, the payee files a criminal complaint before a Judicial Magistrate within one month of the cause of action. Cheque-bounce matters are tried summarily under Section 143 for speed. The court issues summons to the drawer to appear, and Section 139 raises a presumption that the cheque was issued for a debt or liability — the burden then shifts to the drawer to rebut it. If the cheque was issued by a company, Section 141 fixes liability on the persons in charge of and responsible for its conduct. On conviction, the court may order a fine, compensation and/or imprisonment as set out above.

How to legally respond to a cheque bounce incident under Section 138?

A drawer who receives a Section 138 notice should, if the claim is valid, arrange to pay the cheque amount within the 15-day window to avoid prosecution. If the drawer disputes the claim, a prompt written reply to the notice setting out the genuine defence is essential.

Recognised defences include that the cheque was not issued for a legally enforceable debt, that it was given only as security, that payment was already made, that the cheque was materially altered, or that the statutory notice was defective or out of time. The drawer must appear on the date fixed and contest the matter on its merits. Because the offence is compoundable, the parties can also settle at any stage.

Impact and Importance of Section 138

Section 138 is central to protecting creditors and deterring financial misconduct in India. By attaching penalties of up to two years' imprisonment and a fine of up to twice the cheque amount, it makes the cheque a more reliable instrument and gives payees a credible remedy when a cheque is dishonoured.

Protecting Creditor's Rights

A key purpose of Section 138 is to safeguard the payee when a cheque issued to them bounces. It gives creditors a statutory route to recover their dues even where the drawer defaults, deterring drawers from reneging on commitments without consequence. In this way Section 138 supports the credibility of cheques and provides a remedy against loss.

Deterring Financial Misconduct

By criminalising the dishonour of a cheque issued for a debt, Section 138 also deters financial malpractice. The threat of penalty discourages people from issuing cheques they know are likely to bounce, or from using cheques merely to buy time. The provision thereby encourages financial discipline in commercial dealings.

Critical Analysis and Case Studies

Several Supreme Court decisions have shaped how Section 138 is applied:

- In Damodar S. Prabhu v. Sayed Babalal H. (2010), the Supreme Court framed a graded-cost scheme to encourage early compounding of cheque-bounce cases, with rising costs the later a settlement is reached.

- In Dashrath Rupsingh Rathod v. State of Maharashtra (2014), the Court tied jurisdiction to the drawer's bank — a position that Parliament reversed by the 2015 Amendment, which fixes jurisdiction at the payee's bank under Section 142(2).

- In Meters and Instruments Pvt. Ltd. v. Kanchan Mehta (2017), the Court gave directions to expedite Section 138 trials and recognised that many such cases are essentially about recovery of money.

- In Makwana Mangaldas Tulsidas v. State of Gujarat (2020), the Court again stressed speedy disposal of cheque-bounce matters, leading to the suo motu proceedings below.

- In In Re: Expeditious Trial of Cases Under Section 138 of NI Act, 1881 (2021), a Constitution Bench issued comprehensive directions to clear the huge backlog of cheque-bounce cases, including the use of summary trials and limits on converting them to regular trials.

These rulings have made businesses more careful about cheque transactions while keeping the focus on compensating the payee. Concerns remain that the provision is sometimes used to pressure drawers, and the courts continue to balance creditor protection against the risk of misuse.

Recent Amendments and Legal Debates

The most significant recent change is the Negotiable Instruments (Amendment) Act, 2018, in force from 1 September 2018, which added Sections 143A and 148. Section 143A allows a trial court to direct interim compensation of up to 20% of the cheque amount during the trial, while Section 148 allows an appellate court to require a convicted drawer to deposit a further 20% of the compensation before the appeal proceeds. Both measures aim to discourage delay tactics and protect payees.

There has also been a policy debate about decriminalising minor cheque-bounce defaults. In 2020 the Government floated a proposal to decriminalise certain offences, including under Section 138, to reduce the burden on the courts and improve ease of doing business. The proposal drew strong objections from creditors, who argued that the criminal sanction is what gives the cheque its credibility, and it has not been enacted. Section 138 therefore remains a criminal offence.

It is worth noting that the Negotiable Instruments Act itself was not amended by the 2023 criminal-law codes. The substantive offence and timeline under Section 138 are unchanged; only the procedural references shift where the Bharatiya Nagarik Suraksha Sanhita, 2023 has replaced the Code of Criminal Procedure for matters such as the form of complaint and trial.

Conclusion

Section 138 of the Negotiable Instruments Act, 1881 is a cornerstone of commercial law in India. By criminalising the dishonour of a cheque issued for a legally enforceable debt, it strengthens the cheque as a payment instrument and gives payees a fast, time-bound remedy.

The mechanism is precise: present the cheque within its validity, send a written demand within 30 days of the return memo, allow the drawer 15 days to pay, and — if unpaid — file the complaint within one month of the cause of action. Penalties extend to two years' imprisonment or a fine up to twice the cheque amount, and the 2018 Amendment added interim compensation and appellate deposits to deter delay.

The offence is non-cognizable, bailable and compoundable, reflecting its quasi-civil character and the law's preference for settlement over imprisonment. While debates about decriminalising minor defaults continue, Section 138 remains a vital and actively enforced provision for regulating cheque-based transactions in India.